Lender Strategy | Philippine SME Financing Guide

NBFI vs. Bank Loan in the Philippines: How to Pitch Your Management Meeting to Either Lender Type

A Comparative Guide for Philippine SME Founders

By Adriel Maniego · Updated June 23, 2026

The short version

An NBFI loan and a bank loan in the Philippines look like the same product from the outside. They are not. NBFIs decide in days through a principal in the room; banks decide in weeks through committees behind closed doors. The pitch that works in one room actively damages your application in the other. Seven structural dimensions separate them — four learnable from this article, three that require bespoke preparation. Know which room you are walking into before you walk in.

About

Buhay Platforms Inc. is a SEC-registered fintech firm (Reg. No. 2025010186147-22) and a Manila Bulletin Newsmaker of the Year. 100+ financing deals supported nationwide. Network of 30+ financial institutions — commercial banks, rural banks, and non-bank financial institutions. Accredited by the Quezon City, Cebu, Metro Angeles, Pampanga, and Manila Chambers of Commerce and Industry.

Most Philippine SME owners prepare for a lender management meeting the same way regardless of who is across the table. One pitch deck. One financial pack. One mental approach. They wonder afterwards why the NBFI conversation went directly to a term sheet while the bank conversation produced three weeks of silence followed by additional document requests.

The two meetings look similar from the outside. They are not the same meeting.

Why No One Else Is Publishing This

Before walking through the seven dimensions of difference, it is worth naming something most founders never consider: no other type of firm in the Philippine market is structurally positioned to publish this kind of guidance honestly.

Banks will not. The relationship manager you are pitching has limited visibility into the credit committee that will actually decide. Even if the bank understood its own process completely, explaining it would erode the negotiating leverage that opacity provides.

NBFIs will not. Their pricing premium depends on founders being grateful for speed, not on founders calibrating that speed against bank alternatives. A founder who arrives with sharp questions about comparable rates is harder to upsell.

Fintech and platform companies will not. Their entire business model depends on standardizing credit decisions and removing human conversations from the process. They cannot publish guidance on a credit-committee meeting because they have built away from credit-committee meetings entirely.

Traditional advisors will not. Their relationships with one or two banks define their referral pipeline. Honest guidance about which banks are wrong for which founders would damage the institutional relationships their business depends on.

Buhay sits in a different position. Buhay works with a network of 30+ financial institutions across both lender types, and has scoped more than 3,000 companies. We are paid to match the right founder to the right lender for the right moment — not to push any single institution’s product. That position is what makes the rest of this article possible.

Recognise the room you are in. Then recognise that the conversation that gets you through that room is not one you can learn from anyone with a financial interest in the answer.

A Few Definitions Before We Start

- NBFI

- Non-Bank Financial Institution. Includes financing companies, lending corporations, and investment houses. Regulated, but operates with more flexibility than a bank.

- Relationship Manager (RM)

- A bank employee who handles the borrower-facing side of the relationship. The RM is not the decision-maker — they prepare your application for a credit committee.

- Credit Committee

- A group of bank officers who decide on loan applications. Larger banks have multiple committees that an application must pass through in sequence.

- AFS (Audited Financial Statements)

- Annual financial statements signed off by a third-party auditor. The primary document banks underwrite against.

- ADB (Average Daily Balance)

- The average closing balance of your bank account across a period. NBFIs read this as a primary signal of business cash-flow health.

- DSO (Days Sales Outstanding)

- The average number of days between issuing an invoice and collecting payment. A leading indicator of working-capital pressure.

- BIR Form 2316

- The Bureau of Internal Revenue certificate of compensation tax withheld. Standard documentation required by Philippine banks for principals and key owners.

- CMAP

- Credit Management Association of the Philippines — the industry body that maintains shared credit information across member institutions.

- NFIS

- Negative File Information System — a BSP-supervised database of adverse credit records. A negative entry is one of the fastest reasons for a bank application to be declined.

Part One — What Can Be Taught

The four structural dimensions of difference are facts about how each institution is built. They do not change based on your business profile or the personality of the person across the table. They can be learned, internalized, and applied.

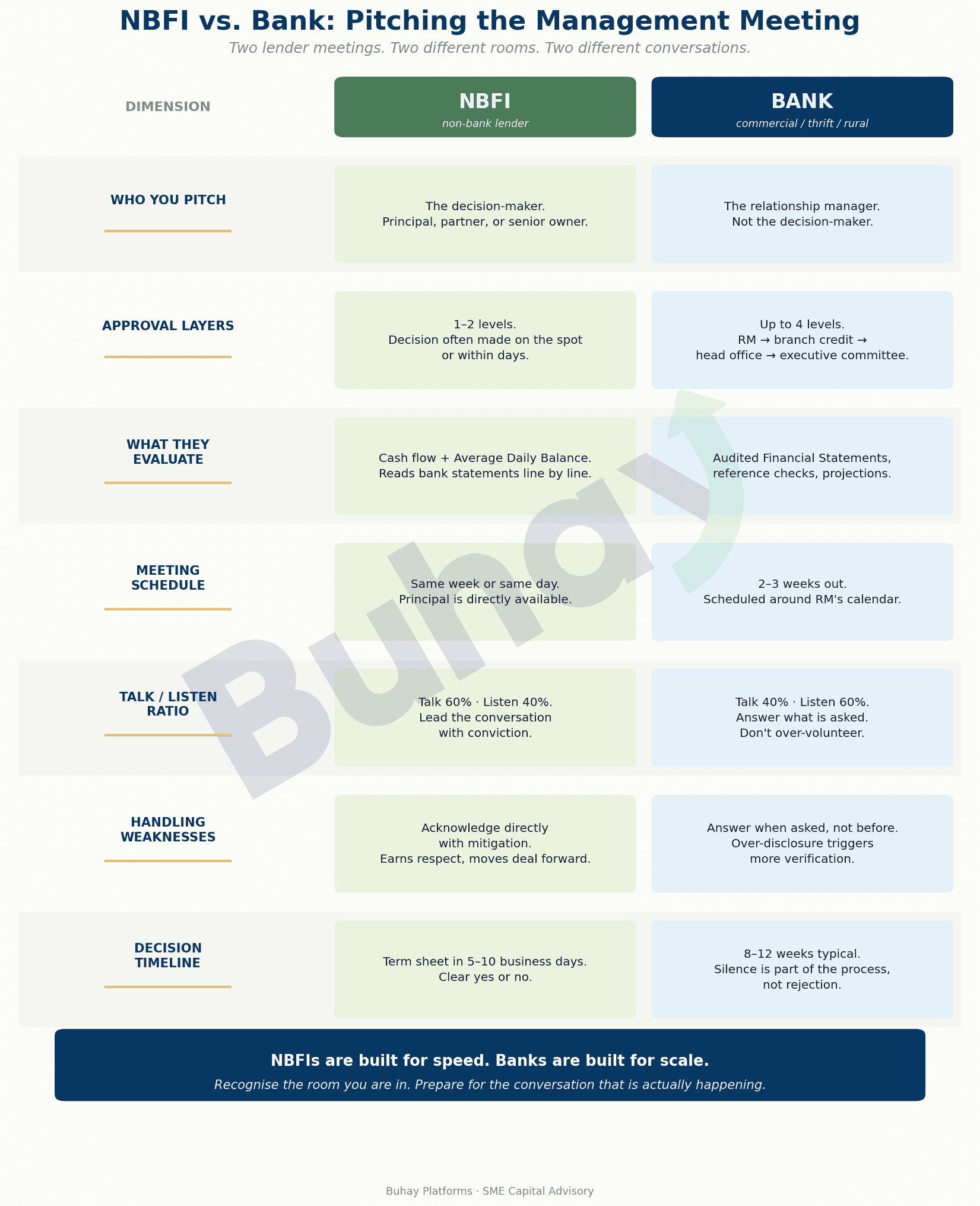

1. Who You Pitch

NBFI: the decision-maker is in the room. Bank: the decision-maker has never met you.

The single most important difference between an NBFI and a bank management meeting is who sits across from you. In an NBFI meeting, you are pitching to the people who will decide. The principal, a partner, or a senior management team member is in the room — and they are evaluating your business in real time. They will interrupt with sharp questions. They will mark up your bank statements as you speak.

In a bank meeting, you are pitching to the relationship manager. The RM’s job is to gather information, document it, and present your application to a credit committee you will never meet. The decision rests with that committee — sometimes two, sometimes three or four levels of approval authority depending on the facility size and the institution.

Your job in a bank meeting is not to convince the RM personally. It is to give the RM the materials to convince three more people who have never met you.

2. Approval Layers

NBFI: 1–2 layers, often within days. Bank: up to 4 layers, often over weeks.

An NBFI typically has one or two levels of approval authority. The principal you are meeting with may have the authority to commit on the spot, or may need to confirm with one partner. Either way, the decision is made by people who have either met you or who will see your file within days of the meeting.

A bank facility can pass through up to four levels of approval: the relationship manager reviews and recommends; the branch or regional credit officer reviews and recommends; the head-office credit committee reviews and decides; and for larger facilities, an executive or board credit committee may also review. Each layer brings its own concerns, its own preferred risk lens, and its own timeline.

The practical implication is that you are not pitching one person in a bank meeting. You are equipping the RM to pitch your deal three more times.

3. What They Evaluate

NBFI: cash flow and ADB read in real time. Bank: AFS, references, and projections documented in depth.

NBFI underwriting focuses on cash flow and Average Daily Balance. The principal will read your last six months of bank statements line by line, looking for the rhythm of money moving through your business — consistent deposits, predictable patterns, a working business that turns over capital. Your AFS matters, but it is secondary.

Bank underwriting focuses on the Audited Financial Statements, reference checks, and forward-looking projections. The credit committee will read three years of AFS for consistency, compare them against your BIR returns and your bank deposits, call your major suppliers and largest buyers, and run a CMAP and NFIS check.

Across the deals Buhay has structured in the past 12 months, the documentation requirement for a bank facility is roughly four times that of a comparable NBFI facility. NBFIs underwrite the present; banks underwrite the documented past, projected forward.

4. Meeting Schedule

NBFI: same week, sometimes same day. Bank: 2–3 weeks out, on the RM’s calendar.

NBFIs typically respond within 48 hours and can offer a meeting within the same week. The principal is usually directly available, because that is who you are pitching. Speed is a feature of how the institution is built.

Banks operate on the relationship manager’s calendar, which means meetings are scheduled around the RM’s existing portfolio commitments — typically two to three weeks out. The RM also determines whether additional bank personnel need to attend, which can add another week.

Plan your preparation timeline accordingly. Never let a delay in bank scheduling stop you from advancing other conversations in parallel.

Part Two — What Cannot Be Taught in an Article

The first four dimensions are structural — how each institution operates. The last three are different. They are not facts about institutions; they are judgment calls about conversations. How much you talk versus listen. When and how to acknowledge a weakness. How to read the silence that follows a bank meeting and respond correctly to it. These are not rules — they are calibrations, and the calibration depends on your business profile, the personality of the lender across the table, and what they specifically need to hear in that specific moment.

Most financial firms in the Philippines treat these as boxes to fit you into — generic advice, templated scripts, the same playbook regardless of who you are. That is the easy version. It is also the version that gets founders rejected by banks they should have been approved by, and overcommitted to NBFIs they should have negotiated harder with.

What We Do Not Publish — and Why

The remaining three dimensions are talk/listen ratio, handling weaknesses, and decision timeline. The figure above gives the one-line version of each — but the playbook behind them, how much, when, and for whom, we do not publish, for two reasons.

First, published advice on these dimensions degrades the moment it is widely read. Lenders are pattern readers. NBFI principals and bank RMs have seen every off-the-shelf playbook circulating in the market. A founder who arrives with the same playbook everyone else is using is immediately recognizable — the advice that helps the first few readers stops helping the moment it becomes generic.

Second, the right calibration is genuinely specific. The right talk/listen ratio for a manufacturer pitching a thrift bank in Cebu is not the right ratio for an exporter pitching a universal bank in Makati. The right way to acknowledge a weakness depends on what the weakness actually is, how recent it was, and what the lender’s other exposures look like. A blog post cannot make those distinctions. A conversation can.

What We Offer Instead

If you are preparing for a management meeting with an NBFI or a bank in the next 60 days, we work directly with founders to prepare for the specific conversation that is actually about to happen. That work includes:

- A pre-meeting assessment of your business profile against the specific lender’s underwriting preferences and committee dynamics.

- Two scenario walkthroughs — one for the lender type you are meeting, one for the type you are not — with annotated dialogue calibrated to your business.

- Real-time preparation for the meeting itself: the talk/listen calibration, the weakness-disclosure plan, and the follow-up timeline appropriate to that institution.

- A debrief after the meeting to refine the approach for follow-ups or parallel lender discussions.

This is not a course and not a downloadable checklist. It is direct work with our team in the weeks before your meeting — because the situations are genuinely unique, and because the alternative, generic advice published as a marketing tactic, actively damages the founders who rely on it.

The Principle Behind the Difference

NBFIs are built for speed. They charge for it. Banks are built for scale. They underwrite for it. The two institutions are solving different problems with different operating models, and the management meeting in each case is a different conversation because of how each institution is built.

The first four dimensions can be learned from an article — they are facts about institutions, and facts can be taught. The last three cannot. They are judgments about conversations, and judgments require depth that an article cannot provide — and that no other type of firm in this market is positioned to offer honestly.

“Recognise the room you are in. Then recognise that the conversation that gets you through it is not one you can learn from anyone with a financial interest in the answer.”

Frequently Asked Questions About NBFI vs. Bank Loans in the Philippines

NBFIs process faster and require less documentation than commercial banks but typically charge higher rates. An NBFI decision is made by a principal in the room over one to two committee layers within days. A bank decision is made by a credit committee escalated through up to four approval layers over eight to twelve weeks. The two products price for different costs of capital and serve different timing needs.

Choose an NBFI when speed matters more than rate — processing takes days versus months. Choose an NBFI when documentation is light or the revenue and declared income gap means a commercial bank cannot yet underwrite the facility size needed. The rate premium is the price of access and speed. For most growing Philippine SMEs, the answer is both at different moments, not one or the other.

Five to ten business days in the right NBFI network — sometimes the same week. The principal is the decision-maker, the underwriting is read on cash flow and Average Daily Balance in real time, and a term sheet typically arrives within two to three weeks of the first meeting if the deal is going to happen. Commercial banks take eight to twelve weeks for an equivalent first facility.

No. The NBFI principal wants to read your business in real time — cash flow patterns, deployment velocity, recent transaction behavior. The bank committee wants a credit package they can defend in a closed-room review with people who will never meet you. The pitch that wins one room actively damages the other. Walking into both with the same materials is the most common preparation mistake we see.

Yes. Non-bank financial institutions in the Philippines are regulated by the Bangko Sentral ng Pilipinas (BSP) under specific NBFI frameworks and, depending on structure, by the Securities and Exchange Commission. Institutional NBFIs — the ones a serious SME borrower should be working with — carry primary and secondary licenses, file with regulators, and are subject to capital adequacy and reporting requirements. Informal lenders operating outside this framework are a different category and not the subject of this guide.

Key Takeaways

- NBFI: decision-maker in the room, days to approval. Bank: committee behind closed doors, weeks to approval.

- The pitch that wins one room damages the other. Calibrate before you walk in.

- For most growing Philippine SMEs, the right answer is both lender types at different moments — not one or the other.

Walk Into the Right Room, Prepared

Buhay matches founders to the right lender type for the right moment across a network of 30+ commercial banks, rural banks, and non-bank financial institutions — and prepares them for the specific conversation that is about to happen. Start with a complimentary assessment.

Adriel Maniego

Founder & CEO, Buhay Platforms Inc.

Buhay — Manila Bulletin Newsmaker of the Year

Accredited, QC, Cebu, Metro Angeles, Pampanga & Manila Chambers

[email protected] · [email protected] · buhay.com.ph

SEC Reg. No. 2025010186147-22.

This article is for informational purposes only and does not constitute legal, financial, or investment advice. Readers should consult qualified professionals before making lending decisions. © 2026 Buhay Platforms.